Poultry Imports

- Poultry meat (mainly from Brazil) declined by 16.22% to in Q1 2025. The outbreak of avian influenza on commercial farms contributed to this drop.

Import Statistics (Figures ending June 2025)

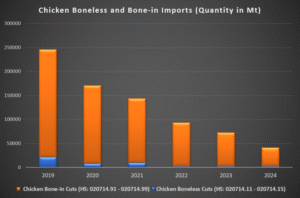

Decline of Poultry Imports 2019-2024

There are public misconceptions surrounding chicken imports and their perceived threat to local production and employment in South Africa.

Historically, there have been instances where local producers had legitimate claims to unfair pricing and issues of chicken dumping. Since the introduction of anti-dumping tariffs, this risk has been mitigated, and poultry imports have seen a sharp cut.

Looking at the latest trade statistics, imports of bone-in portions dropped by 83% from 224,198 tonnes in 2019 to 38,956 tonnes in 2024.

In practice, both domestic poultry production and poultry imports play vital roles within South Africa’s poultry value chain. The meat processing industry sustains approximately 125,000 jobs, while the agricultural poultry sector directly employs around 50,000 people.

However, statistics show that South Africa does not produce enough chicken for domestic consumption. Imported poultry continues to bridge a 20% supply gap that domestic producers cannot fill.

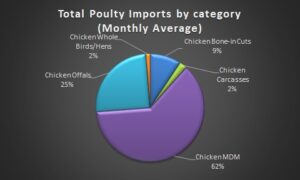

Total Poultry Imports by Category: Jan-May 2025

Poultry Exports

- The EU, UK, and Saudi Arabia remain key targets for South African poultry exports, particularly cooked breast meat. However, due to phytosanitary restrictions uncooked chicken exports are not anticipated at this stage.

- Inspections by the UK and Saudi Arabia are underway, and residue monitoring programmes have been submitted.

- For the year ending June 2025, total chicken exports decreased by 19% year-on-year, totalling 51,888 metric tonnes, with bone-in chicken leading the export category. SA-origin exports decreased by 6% YoY, totalling 37,932 metric tonnes.

Export Statistics (Figures ending June 2025)

South Africa’s Chicken Exports 2021-2024

International Poultry Markets

Import bans on Brazilian chicken have disrupted global poultry markets, leading to higher prices for mechanically deboned meat (MDM) in South Africa.

Recent media reports indicate MDM import prices there have doubled and rising USDA prices suggest global MDM costs will likely stay high in the near term.

Local Market

Multiple outbreaks in the Northern Hemisphere threaten South Africa’s poultry industry, as the virus migrates with wild birds from Europe in winter, causing infections to rise. Large-scale vaccination programmes are key to reducing future risks.

Local poultry prices remain high due to reduced supply after issues at Daybreak and a ban on imports from Brazil. Elevated prices are expected to persist until the end of Q3.

June 2025 Poultry Prices

| Poultry Product | Price (R/kg) | w/w Change | m/m Change | y/y Change |

| SA Whole Bird, Frozen | R35.66 | +2.4% | +1.6% | +1.1% |

| SA Whole Bird, Fresh | R40.71 | +1.3% | +7.5% | +17.2% |

| SA Individually Quick Frozen (IQF) | R35.49 | +0.5% | +2.6% | +19.3% |

ABSA AgriTrends Livestock Report 12 June 2025

Chicken Price Forecasts (2026-2027)

| Year | Frozen Whole Bird R/kg | Fresh Whole Bird R/kg | IQF R/kg |

| 2026 | 35.58 | 37.00 | 33.62 |

| 2027 | 35.80 | 37.52 | 34.10 |

Source: Absa AgriBusiness, 2025

Outlook

Local poultry prices are expected to rise due to firm global prices tied to disease concerns, lower supply, and exchange rate effects.

After stabilising at higher levels post-2023, continued high input costs have squeezed producer margins.

Weak demand, especially among lower-income consumers, has restricted price adjustments despite expensive feed.

Prices may ease slightly as feed and global prices decline, though ongoing disease issues could reverse this trend.

Lower feed costs are projected to improve margins and encourage supply in the second half of 2025, likely moderating medium-term price increases.

Impact: Brazil’s First Bird Flu Outbreak

On 15 May, Brazil’s confirmed the presence of highly pathogenic avian influenza (HPAI) in a commercial poultry farm in Montenegro, Rio Grande do Sul.

South Africa’s Department of Agriculture, Land Reform and Rural Development (DALRRD) placed an immediate blanket ban as a standard bio-security protocol when a regionalisation agreement is not in place. Brazilian import bans were backdated to poultry products packed on or after 01 May 2025.

Brazil accounts for 92% of the country’s mechanically de-boned meat (MDM), importing an average of 18,000 metric tonnes per month. It also supplies 73% of other poultry imports, including chicken offals and bone-in chicken.

After a two-month halt in poultry trade, DALRRD officially reopened import permits for poultry from Brazil on 4 July 2025.

While DALRRD had announced a regionalised protocol for Brazil on 19 June, no regionalisation agreement was settled on between South Africa and Brazil and therefore no trading took place.

Brazil was officially declared free of avian influenza as of 26 June, and the market was re-opened by DALRRD a week later.

There is still no regionalisation agreement in place between South Africa and Brazil.

Market Impact

The ban, which halted nearly all shipments overnight, has resulted in significant losses:

- An estimated 100 million meals per week were compromised during the suspension, particularly impacting school feeding programmes and low-income households.

- Meat manufacturers experienced layoffs after factories were unable to import MDM for two months.

- MDM prices spiked by 140%, driving up inflation for budget chicken products.

Ongoing Impacts

Even with the ban lifted, it will take 6–8 weeks to replenish supply chains due to shipping and customs delays.

Prices for processed meats are expected to remain high until October, with regular supply and pricing only expected to stabilise by November 2025.

Policy Implications

Industry leaders are pushing for policy certainty and regionalisation protocols which are crucial to mitigating the risk of future food crises.

This would allow imports from unaffected regions during disease outbreaks, as is already practiced with the USA.

Chicken Imports: Market Access

The following markets have recently reopened:

- Denmark (Production dates from 9 May 2025)

- Netherlands (16 May 2025)

- Belgium (6 May 2025)

- Brazil (4 July 2025)

The following markets are currently closed due to disease outbreak:

- Australia (HPAI)

- Canada (HPAI)

- France (HPAI)

- Germany (AFS & HPAI)

- Hungary (HPAI)

- Israel (HPAI)

- New Zealand (HPAI)

- Poland (HPAI)

- Sweden (HPAI)

- United Kingdom (HPAI)

- Zimbabwe (HPAI)

USA States banned for imports

As of July 2025, poultry and poultry products may not be imported from the following 27 regions due to ongoing HPAI concerns:

| Current restricted USA states | |

| Arizona | Montana |

| Arkansas | New Jersey |

| California | New Mexico |

| Colorado | New York |

| Delaware | North Carolina |

| Florida | North Dakota |

| Illinois | Ohio |

| Indiana | Oregon |

| Iowa | Pennsylvania |

| Kansas | Puerto Rico |

| Maryland | South Dakota |

| Michigan | Virginia |

| Minnesota | Wisconsin |

| Mississippi | |