The South African Poultry Association (SAPA) has initiated legal proceedings against the Department of Trade, Industry and Competition (DTIC) after failing to get DTIC’s Minister Parks Tau to scrap the 72 000-tonne annual poultry quota.

The Tariff Rate Quota agreement allows the US to export bone-in chicken to South Africa without anti-dumping duties.

Although a Most Favoured Nation (MFN) tariff of 62% still applies to bone-in chicken, SAPA argues that it cannot compete with “dumped” chicken from the US, and that it should have been scrapped when Donald Trump applied the 30% reciprocal tariffs (later 15%) last year.

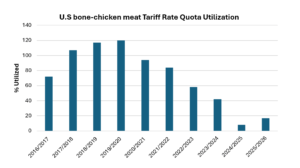

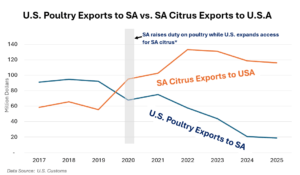

Meanwhile, United States bone-in chicken meat exports to South Africa have been on a decline since March 2020 after the increase in the MFN tariff to 62%.

The legal pursuit comes as bit of mystery, since the AGOA agreement expires at the close of 2026, and the US plans to “reform and modernise” the 2027 AGOA renewal.

Minister Tau is expected to request an extension since he did not file a response in time, and by the time the case reaches court, the existing AGOA agreement will likely have lapsed.

From the DTIC’s perspective, SAPA’s legal action may appear premature, especially given the ongoing Competition Commission investigation into the poultry value chain.

The Minister is unlikely to welcome a parallel court battle that distracts from the Commission’s mandate to examine structural barriers, pricing dynamics and market concentration.

The DTIC may well view the litigation as an attempt to pre‑empt or influence the outcomes of that investigation, particularly where issues of dominance and market power are already under scrutiny.

In this light, the Minister’s reluctance to engage the court process could reflect a preference to allow the Commission’s inquiry to run its course rather than be overshadowed by a dispute over an underutilised quota.

The Quota Utilisation

The quota itself is being vastly underutilised. In 2023, only 28 131 tonnes were shipped. In 2024, that figure dropped to 5 956 tonnes. For 2025, 12 251 tonnes were exported, amounting to 17% of the quota.

Even if the US poultry quota were being fulfilled, the 72 000-tonne allocation represents less than 4% of local production, and 3% of domestic consumption (based on the latest available 2024 production and consumption data).

It is hard to see how serious the threat to local poultry really is, especially given the resources SAPA is spending to challenge the fragile quota. Even so, the case shows how far local producers are prepared to go to protect their dominant market position.

The Bigger AGOA Picture

The greater issue is that the AGOA debate cannot be reduced to a single poultry quota. South Africa’s broader export relationship with the United States carries far higher stakes, particularly for the motor industry and fresh produce exporters, which stand to lose billions in revenue and thousands of jobs if South Africa is excluded from AGOA or receives materially fewer benefits in any renewal.

Agriculture, especially fruits, vegetables and nuts, would be among the sectors most exposed to weaker market access, while the automotive sector remains one of the country’s most significant AGOA beneficiaries.

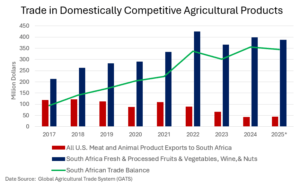

In terms of agricultural trade, South Africa has a lot more to lose. South Africa enjoys a large and growing agricultural trade surplus, especially in products that are considered sensitive because they are produced in both countries.

Overall, the South African agricultural trade surplus has grown from $2 million in 2016 to $264 million in 2025. Meanwhile the surplus in sensitive products has increased from $94 million to $344 million. Further restricting U.S. poultry exports beyond the current very low levels, threatens South Africa’s agricultural export gains.

In this context, pursuing a fight over an underutilised poultry concession risks missing the wider national interest: protecting sectors that generate far greater export earnings, sustain regional economies and support large numbers of workers.

At the same time, AGOA in its current form cannot be treated as a permanent economic crutch. If the United States wants a more reciprocal arrangement in future, South Africa should engage that reality pragmatically rather than act as though preferential access is an entitlement.

South Africa cannot afford to rely indefinitely on a unilateral concession or “handout” to keep its export sector afloat. The more rational long-term response is to use the uncertainty around AGOA as a catalyst for reform: improve competitiveness at home, reduce logistics and infrastructure bottlenecks, deepen value addition, and expand into new markets through stronger global partnerships and deliberate export diversification.

In other words, the priority should not be preserving dependence on Washington, but building a trade strategy that leaves South Africa stronger, more resilient and less vulnerable to the political dispositions of any single partner.

Back to Poultry: Exports

Regardless of the AGOA renewal outcome, we can all agree that poultry exports need to grow for a more competitive poultry sector. At present, poultry producers export only about 3% of output, or roughly 50 000 tonnes a year.

The industry has attributed this weak export performance to industry traders and government shortcomings in implementing the 2019 Poultry Master Plan (PMP), arguing that more state veterinary staff and facilities are needed to issue health certificates for chicken exports.

One could argue that the incentive to export poultry has been negligible since local producers retain the lion’s share of the South African market with no end in sight for heavy trade protections.

It seems, however, that local producers have come to realise the necessity for export growth, recently stating that increased chicken exports have been identified as essential for the poultry industry’s continued growth.

SAPA’s Izaak Breitenbach explains that a renewed export drive is one of the pillars of the revised PMP, signed last month by government, the poultry industry, and meat traders. “The plan is to expand exports from neighbouring states, which take most of South Africa’s chicken exports, to new markets in the Middle East and Europe.”

“We’re not exporting enough,” he said. “We need strategically to change this industry from a local industry to an export industry as well.”

If executed effectively, this strategy could help build a more competitive local poultry industry by expanding revenue streams and reducing reliance on the domestic market alone. It could also create space for imports to play a complementary role, broadening the range of affordable protein options available to consumers, particularly lower-income households in South Africa.

No country is fully self-sufficient. Imports are a global economic reality, and competition between local and imported goods helps curb monopolies, widen consumer choice, and keep prices in check.

The real test is not whether South Africa can wall off its poultry market, but whether it can build one that is competitive enough to export, resilient enough to grow, and balanced enough to serve consumers rather than entrenched interests.