South Africa’s four biggest poultry producers are in the hot seat as the Competition Commission’s inquiry flags industry dominance and barriers to new entrants.

According to Business Day, SA’s major poultry producers will have to justify their business practices as the Competition Commission moves forward with its antitrust investigation.

Astral, RCL, Country Bird, and Sovereign control nearly 63% of South Africa’s poultry market. The sector comprises 973 farms, of which about 680 are large commercial-scale farms.

The inquiry will investigate whether contract grower relationships with these companies involve power imbalances and how this impacts competition and small-scale producers. The probe is planned to commence before the end of 2025.

Despite the SA Poultry Association (SAPA) indicating that it will fully co-operate with the inquiry, it has appealed for “understanding and support” to continue supplying SA with affordable meat protein.

The US Poultry Grievance

Alongside the Anti-Trust Inquiry’s findings, local poultry has maintained a stance that spotlights perceived external challenges. The industry consistently lobbies for tighter restrictions on poultry imports.

In a recent publication, FairPlay, lamented the ‘dangers’ of US chicken imports, suggesting that SA government is secretly negotiating with the US by committing the poultry industry to damaging sacrifices to lower the 30% tariffs on SA exports.

Despite the uncertainty around the AGOA renewal with the US, a Tariff Rate Quota (TRQ) agreement with the USA remains in place for 72,000 tonnes of bone-in chicken per annum.

Poultry imports under this quota are exempt from the 9.40/kg anti-dumping duty applied to U.S. bone-in chicken.

What local poultry lobbyists consistently fail to mention is the 62% general tariff still applicable to US imports, even under the quota.

“When the government allows tens of thousands of tonnes of US chicken to enter South Africa at preferential rates, the threat to local producers is immediate,” says Francois Baird, founder of FairPlay.

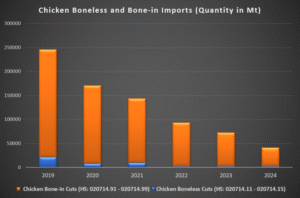

Notably, the 62% most favoured nation (MFN) tariff implemented in 2020 has resulted in a dramatic decrease of bone-in imports over the last 5 years, including imports from the USA under the quota.

In 2024, the United States exported 11,351 tonnes of bone-in chicken to South Africa, representing 16% of the current quota.

The lower export volume is largely attributed to the 62% tariff, which affects the competitiveness of US chicken in the South African market.

Fearing that US imports to SA will continue to expand, Baird asserts that “a significant annual quota of US chicken will enter at dumped prices without any tariff restrictions.”

The statement is speculative and unfounded. Expansion of the annual quota, originally set at 65,000 tonnes in 2010, is based on production vs. consumption, reflecting growth in the market over the last 10 years as published by DALRRD.

The quota expansion since its inception in 2016 amounts to 1% per year on average, for a total of 10%.

Considering the 72,000-tonne quota represents 3.1% of South Africa’s total annual chicken consumption, fear-driven speculations around the US quota and ‘dumping’ is wholly unsupported.

The US quota remains subject to the 62% MFN tariff, contrary to the lobbied assertions of US imports being tariff-free.

The MFN duties are applicable to chicken imports from all countries except the EU, the UK and SADC nations:

- Frozen offal (heads, livers, feet): 30%

- Frozen carcasses: 31%

- Frozen boneless portions: 42%

- Frozen bone-in portions: 62%

- Whole frozen chicken: 82%

Anti-Competitive Sentiment

South Africa imports chicken to fill a 15% gap in domestic consumption, with local production unable to meet demand.

South Africa imported 398,000 tonnes of chicken last year, of which 239,000 tonnes representing 61%, was mechanically deboned meat (MDM).

MDM is a paste-like poultry product imported to produce processed meats including polony and vienna sausages. MDM is not produced commercially in South Africa and is not subject to general or anti-dumping duties.

The remaining 38% of poultry imports primary consists of chicken offals at 24%. Whole birds and carcasses make up 4%, while bone-in cuts make up 11%.

In practice, both domestic poultry production and poultry imports play vital roles within South Africa’s poultry value chain. The meat processing industry sustains approximately 125,000 jobs, while the agricultural poultry sector directly employs around 50,000 people.

Rural farmers remain unaffected by imports, continuing to sell live birds locally with negligible exposure to imported poultry.

Besides the fact that poultry imports don’t displace domestic product, it provides a more affordable protein alternative for consumers with low disposable income.

In the latest issue of Poultry Bulletin, SAPA has openly prioritised ‘ending the 72,000 tonne annual US import quota’.

What are the underlying reasons for the local poultry’s focus on restricting bone-in poultry imports? At what point will the industry showcase an ability to compete effectively in the market?

The industry’s palpable anti-imports sentiment lends further credibility to the Competition Commission’s investigation into industry dominance.

Export Ambitions Stalled

According to SAPA, some progress has been made in advancing exports of cooked chicken products to the EU, UK, UAE, and Saudi Arabia.

However, the poultry industry is directing criticism at the government for failing to deliver on prerequisites necessary to grow poultry exports, as envisioned in the Poultry Master Plan (PMP).

“The master plan envisaged an exports bonanza, with chicken exports doubling and trebling in a decade. However, a lack of government support – at home by the failure to invest in the veterinary facilities needed to certify exports, and abroad by a failure to pursue rigorously the opening of new markets for South African chicken – has squandered much of that opportunity,” says FairPlay.

The Master Plan made government directly responsible for securing veterinary protocols, including upgrading animal health systems and certification capacity to safeguard exports.

“Export negotiations have stalled, leaving producers who invested in world-class cold chain and processing facilities with no new markets to sell to. Veterinary laboratories, essential for issuing internationally recognised health certificates, remain underfunded and understaffed,” SAPA said in a statement issued last month.

While SAPA and the State point fingers at each other, the question is whether there is genuine resolve to export poultry meaningfully at all?

While South Africa’s red meat sector exports globally despite its own challenges, why does SA poultry lag behind?

The government has repeatedly and unsurprisingly fallen short of expectations, whereas local poultry focusses heavily on lobbying for stricter import regulations to preserve their dominant position in the market.

As South Africa faces the implications of the 30% US tariffs imposed on key agricultural exports, it is pertinent to examine our own trade policies, such as MFN import duties that reach up to 82% on poultry products.

How can poultry producers presume to export while pushing for tighter import controls?

On paper, the export ambitions of the PMP do not correspond with action by government, and little more from the poultry industry.

The bottom line is the sector will not achieve sustainable growth that benefits all stakeholders, including vulnerable consumers, until there is collaborative alignment between government, trade, and industry.